Fragile Shield

For years, India’s economic story has rested on a comforting assumption: that strong domestic demand can insulate the country from global turmoil.

Synchronous movement in industrial and monetary metals is indicating that markets are pricing both growth expectations and financial instability simultaneously, a late-cycle configuration that historically resolves through sharp, disruptive corrections.

(Photo: Xinhua via IANS)

Gold, silver and copper are all trading at or near record levels. Gold has surged past $4,600 an ounce, silver crossed $90, and copper has breached $13,000 per tonne. In India, gold is near ₹1.45 lakh per 10 grams and silver above ₹3 lakh per kilogram.

On the surface, this looks like a straightforward commodity supercycle, driven by electrification, artificial intelligence, energy transition and supply constraints. But that explanation is incomplete. What markets are actually pricing is more subtle, and potentially more concerning.

Advertisement

They are pricing two incompatible macro-outcomes at the same time.

Advertisement

Industrial metals like copper typically rise when investors are confident about growth. Precious metals like gold rise when confidence in financial stability, currencies or policy credibility weakens. Seeing both surge together, and with such force, is not a normal mid-cycle configuration. It is a sign of unresolved macro tension.

Growth optimism and monetary anxiety together

One part of the rally reflects belief in sustained capital expenditure. Power grids, data centres, electric vehicles and defence-linked infrastructure are genuine demand drivers, particularly for copper and silver.

But the simultaneous surge in gold points to something else, rising demand for monetary insurance. This reflects geopolitical risk, high leverage across financial systems, and uncertainty about the path of liquidity as global monetary policy tightens in real terms, even if nominal rates pause.

Markets are not choosing between these futures yet. They are hedging both. Such configurations tend to emerge late in the cycle, when growth has not collapsed but confidence in its durability has weakened. Investors are still willing to hold cyclical exposure, but they no longer trust the financial backdrop enough to do so without insurance.

Why financial flows matter more than physical demand

This rally is being driven less by immediate physical shortages and more by financial positioning. Industrial demand does not change overnight across the entire metals complex. Nor do supply constraints suddenly bind everywhere at once.

What does adjust rapidly is capital allocation. Exchange-traded products and futures markets now dominate marginal flows into commodities. As a result, metals have increasingly become macro instruments, used to express views on inflation, liquidity, geopolitics and risk sentiment.

This creates a paradox. Investors believe they are moving into real assets to hedge instability, but they are doing so largely through paper claims. These exposures remain vulnerable to margin calls, funding stress and volatility spikes, the very conditions they are meant to hedge against.

Silver is where the stress becomes visible first

Silver sits at the fault line between industry and money. That makes it unusually sensitive to shifts in market psychology, and a useful early-warning signal.

In recent months, strains have emerged between paper and physical silver markets. Physical hubs in Asia have traded at persistent premia to international benchmarks. Domestic prices in Mumbai have at times been 5 to 12 percent higher than global references, reflecting tightness in deliverable metal rather than speculative excess.

Short-dated silver lease rates have also spiked sharply from their normally subdued levels, indicating stress in market plumbing. These are not signs of imminent breakdown, but they are classic markers of strain. Similar patterns appeared ahead of broader dislocations in 2008 and again during the liquidity shock of March 2020.

How these phases usually resolve

History suggests that such equilibria rarely last.

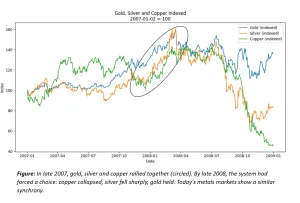

Ahead of the 2008 financial crisis, commodities rallied broadly on a real-assets narrative. When funding markets seized, the unwind was brutal. Copper collapsed as growth expectations reset. Gold initially fell as investors sold liquid assets to raise cash, then stabilised earlier once forced liquidation passed. Silver experienced the most volatility of all.

The 1970s offer a different backdrop but a similar lesson. Inflation and geopolitical stress lifted hard assets together, until recession forced a separation. Industrial commodities weakened, while gold retained its monetary premium.

Today’s market structure adds a new twist. Financial flows are faster, leverage is embedded through multiple layers of the system, and exits can narrow abruptly once volatility rises. That raises the risk of sharper, more discontinuous adjustments.

The implications for India

For India, this broad metals rally matters concretely. Imported metals feed directly into inflation and raise input costs for power equipment, electronics and infrastructure. Copper-intensive sectors such as renewable energy, electric vehicles and grid expansion face margin pressure just as policy pushes for accelerated deployment. Higher metal prices also have an impact on the current account at a time when energy and commodity prices are already elevated.

Household balance sheets are affected too. Indian households hold an estimated 25,000 tonnes of gold. When prices surge, wealth effects can temporarily boost consumption, even as high prices defer jewellery demand and alter savings behaviour. Retail participation in silver has accelerated sharply, with many investors treating it as a leveraged expression of both growth optimism and macro anxiety. That positioning increases vulnerability if sentiment shifts abruptly.

What investors should take away

The key message is not that a crisis is inevitable. Many late-cycle tensions resolve without systemic disruption. But metals are often early messengers. They sit at the intersection of the real economy and financial markets, and they tend to reflect stress before it appears in credit spreads, funding markets or official data.

When gold and copper surge together, markets are signalling uncertainty, not conviction. When silver begins to show physical tightness alongside financial exuberance, it suggests fragility is accumulating beneath the surface.

For investors, the implication is not to abandon commodities, but to recognise what they are really pricing. In environments like this, volatility is information. By the time stress becomes visible elsewhere, repositioning is usually already under way.

(The author is Faculty of Finance at Bhavan’s SPJIMR. He holds Ph.D. Economics from IIM Calcutta, MBA from IIM Calcutta, and B. Tech from IIT Kharagpur.)

Advertisement